Mastering Your Money: The Power of Budgeting

Learn how to build a realistic budget that helps you stay on track, reduce stress, and reach your financial goals. Budgeting doesn’t mean giving up everything you enjoy—it means knowing where your money is going so you can make confident decisions. Discover how to take control of your finances and unlock a future of financial freedom!

Creating a Budget

A budget is simply a plan for how you’ll use your money each month. It helps you cover essential expenses, prepare for unexpected costs, and save for goals that matter to you. If you’ve ever wondered where your money went at the end of the month, budgeting is the first step to getting clarity. It gives you clarity and confidence with your money, enabling you to make intentional choices and work toward your most important goals. Explore how to get started, identify income, track expenses, and ensure your budget evolves with you. The goal isn’t perfect control, but feeling confident and informed.

Getting Started

Before We Begin You’ll Need:

- Recent pay stubs or income records to confirm your earnings.

- Bank and credit card statements (last 1-2 months) to see your spending.

- A calculator or spreadsheet to help with calculations.

- A budgeting app, if you prefer digital tools for tracking.

- Just honest numbers are needed, not perfection.

On This Page:

Why is Budgeting Important?

- Uncover Savings Oppurtunities

- Stay in Control of Your Money

- Support Financial Goals

- Reduce Stress

Identify Your Income Sources

Earned Income

The income you receive directly from your hard work. Think of your regular salary or wages from a job, or even military pay if applicable.

Passive Income

This can include earnings from investments like dividends or interest, or rental income if you own property. It’s money that works for you.

Additional Income

This is consistent but less conventional payments. This could be alimony from a former spouse, child support payments, or even retirement income.

Government Support

This includes public assistance benefits, Social Security payments (whether retirement, survivor, or dependent benefits), or disability-related income.

Envelope Method

What to Spend Money On?

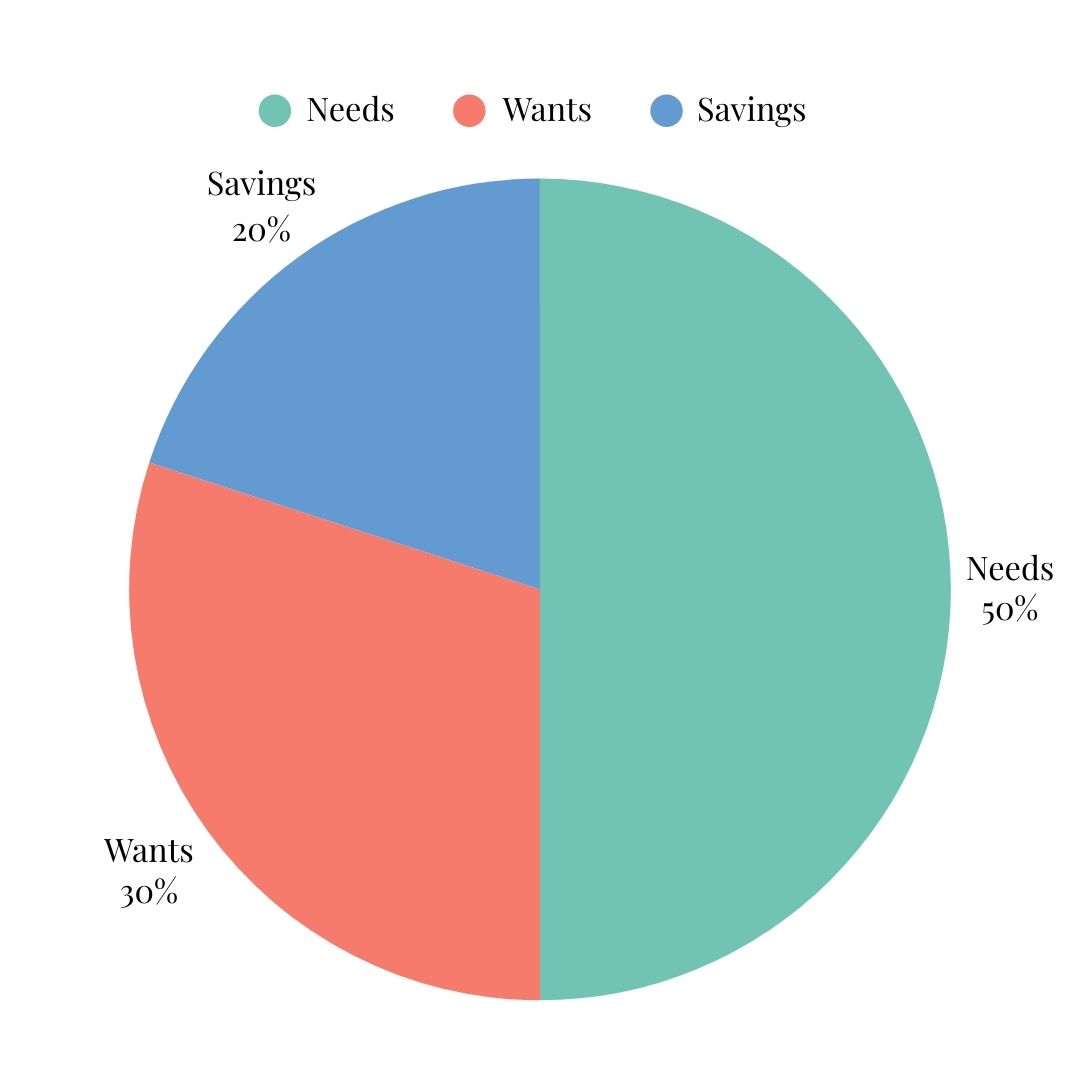

50-30-20 Rule